By:

Beckett Cantley

Geoffrey Dietrich

President Biden sent ripples through the financial world when he proposed a “once-in-a-generation” investment in the foundations of middle-class prosperity [1] with a tax reform agenda set to neutralize the wealth disparity in our country.

President Biden sent ripples through the financial world when he proposed a “once-in-a-generation” investment in the foundations of middle-class prosperity [1] with a tax reform agenda set to neutralize the wealth disparity in our country.

From the outset, it is vitally important to recognize that “tax” is a multi-layered conversation and, depending on the facts used, any conversation about tax will have different outcomes. This article does not attempt to fully explore all facts. Instead, it seeks to start a conversation and aid in understanding the proposed agenda. Thus, first we will touch on some facts related to the actual amounts of tax paid by the wealthy. Next, we discus the capital and ordinary income tax proposals raised in the AFP. Finally, we explore some potential outcomes if the AFP is passed into law.

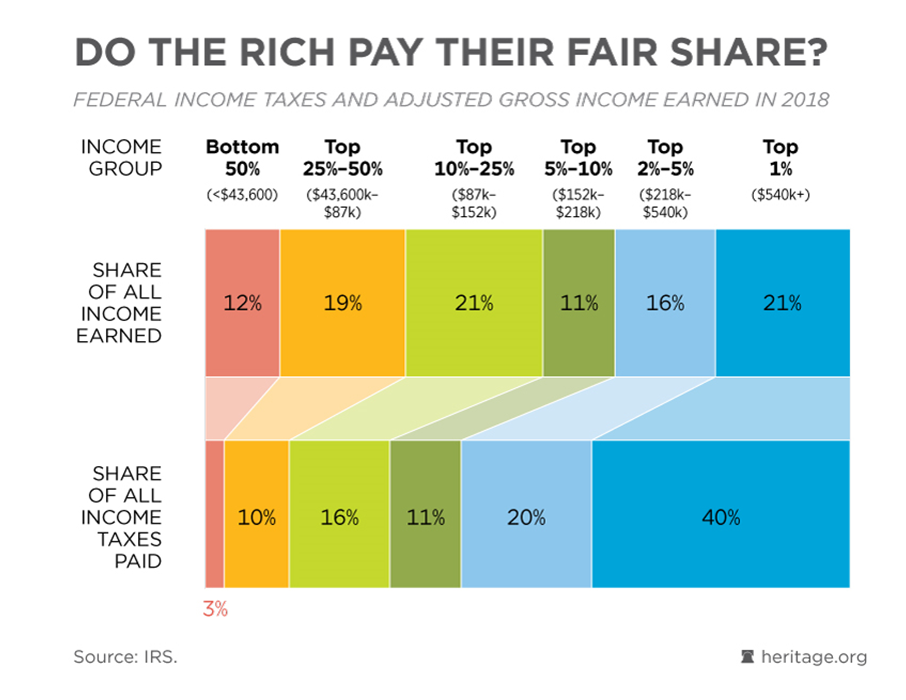

President Biden has said, on several occasions, that America’s wealthy need to “just pay their fair share.” While we recognize most Americans distrust the tax system (and in many cases, government generally), most Americans do believe they should pay “something” in tax. After all, this is the greatest nation in the world with access to public services, including free schooling for our children, and rights, such as free speech, which we often take for granted. Most Americans’ views start to differ when “fair share” becomes a rally cry with reports on billionaires qualifying for certain tax credits reserved to the poor. Again, not to delve into the probably-completely-legal-and-ethical means by which corporations and their owners manage taxation, we present the following graphic from the Heritage Foundation :

Beckett Cantley

Geoffrey Dietrich

President Biden sent ripples through the financial world when he proposed a “once-in-a-generation” investment in the foundations of middle-class prosperity [1] with a tax reform agenda set to neutralize the wealth disparity in our country.

What is the Intent of the Biden American Families Plan?

The proposed agenda in the American Families Plan (“AFP”) marks an ambitious proposal to reconfigure both how the United States rewards the American Dream and how it proposes to roll out enough social programs to solve what ails our country. It proposes paying for those programs with an equally ambitious plan to tax the wealthy in ways heretofore unimagined—or if imagined, previously unattainable.From the outset, it is vitally important to recognize that “tax” is a multi-layered conversation and, depending on the facts used, any conversation about tax will have different outcomes. This article does not attempt to fully explore all facts. Instead, it seeks to start a conversation and aid in understanding the proposed agenda. Thus, first we will touch on some facts related to the actual amounts of tax paid by the wealthy. Next, we discus the capital and ordinary income tax proposals raised in the AFP. Finally, we explore some potential outcomes if the AFP is passed into law.

President Biden has said, on several occasions, that America’s wealthy need to “just pay their fair share.” While we recognize most Americans distrust the tax system (and in many cases, government generally), most Americans do believe they should pay “something” in tax. After all, this is the greatest nation in the world with access to public services, including free schooling for our children, and rights, such as free speech, which we often take for granted. Most Americans’ views start to differ when “fair share” becomes a rally cry with reports on billionaires qualifying for certain tax credits reserved to the poor. Again, not to delve into the probably-completely-legal-and-ethical means by which corporations and their owners manage taxation, we present the following graphic from the Heritage Foundation :

As shown above, the “wealthy” (limited to only the top 1%) pay a staggering 40% of all tax revenue, as reported by the IRS. When you include those Americans making above $200,000 per year as “wealthy,” it becomes 60%. This is after the 2017 Tax Cuts and Jobs Act “reduced tax bills for the lowest-income Americans by 10% while only cutting taxes for the top 1% by 0.04%” according to the Heritage Foundation. Reasonable minds may differ on what “fair share” amounts to, as—arguably—certain demographics are able to take greater advantage of the tax system than others.

Corporations with sufficient revenue at risk are likely to go offshore (again) to take advantage of better tax treaties. Apple’s (and others’) use of the Dutch-Irish Sandwich should provide a good example of the lengths a corporation will go to limit or reduce taxation by even just small percentages.

The truly wealthy are likely to move assets and income to creditor protection jurisdictions and take advantage of legitimate investments with income tax benefits for their investments and wealth. Individuals will find other ways to pass income and transfer wealth or push off selling businesses/stock/houses/etc. The tax on the wealthy may face significant hiccups in tax collection, even with a doubled budget for the IRS. This could be why the Biden Administration is putting such a priority on global corporate and minimum taxes. With all the tax minimization options available to wealthy individuals, it is questionable how we will pay for these social programs.

If you have clients in the upper income brackets who share these concerns, the attorneys at Cantley Dietrich would enjoy having a conversation with you about how you can protect them from some of the challenges they will likely face in the next few years.

How Does the AFP Tax Plan Attack the Wealthy

The AFP Tax Plan promises to improve life for all Americans with increased taxation on the wealthiest Americans without compliantly reduced taxable income. It is nearly impossible to keep current with the proposals and all their changes, so we focus on four tax points discussed regularly and the wealth neutralizers “hidden” in plain sight.

- First, the Biden Administration proposes raising the top marginal income tax rate from 37% to 39.6%. This would apply to income over $452,700 for single or head of household filers and $509,300 for joint filers. This is not good news for well-compensated individuals or joint income families entering the top tax bracket approximately $105,000 sooner than they would otherwise.

- Next, the Biden Administration proposes taxing long-term capital gains and qualified dividends at the ordinary income rates for taxpayers with taxable income above $1 million. When combined with the proposed new top marginal rate of 39.6% and the 3.8% Net Investment Income Tax (“NIIT”)—the flat tax affectionately known as the “Obamacare Surcharge”—the top marginal rate becomes a whopping 43.4% .

- We uncover a “hidden” attack on your wealth in the tax on unrealized gains at death above $1 million ($2 million for joint filers, plus the current law capital gains exclusion of $250,000/$500,000 for primary residences). This is a rally point for the advocates of closing tax “loopholes.” Sadly, many Americans —especially middle-class taxpayers—pass wealth by transferring appreciated property upon the death of a loved one. The transfer of a family home, family farms, or other appreciated property with low basis upon the death of a loved one would become a target-rich environment of previously untouchable gains.

- The final attack we uncover is hiding in the expansion of previous taxation to which we have already grown accustomed. In addition to the other points previously discussed, the Plan would apply the NIIT 3.8% to active pass-through business income above $400,000. This wealth neutralizer hides in plain sight in a proposal to close perceived “gaps” in the tax law between the FICA and SECA taxes. There are currently four identified “gaps”:

- distributions to active S corporation shareholders;

- distributions to active limited partners;

- gains from the sale of business property from active non-trading businesses (like an MRI machine used by a radiology practice or a truck used by a construction company) which might not be subject to NIIT for active partners in the business; and

- active LLC members.

How Might the AFP Tax Plan Do More Harm Than Good

The Administration makes its projections on eight (or ten) year plans for revenue. However, the revenue to be raised requires fifteen years to reach its funding goal (in a vacuum). Thus, the AFP begins with a five-to-seven-year shortfall. Unfortunately, even if the laws backdate eligibility or claw back income to fall under the future laws, it is unlikely to catch everyone. We wonder how many Fortune-level companies will pay their Big 4 accounting firms to find a way to pay some tax in year one only to plan an escape after that? If some of the biggest companies do so, the AFP loses tax dollars during the next nine tax years.Corporations with sufficient revenue at risk are likely to go offshore (again) to take advantage of better tax treaties. Apple’s (and others’) use of the Dutch-Irish Sandwich should provide a good example of the lengths a corporation will go to limit or reduce taxation by even just small percentages.

The truly wealthy are likely to move assets and income to creditor protection jurisdictions and take advantage of legitimate investments with income tax benefits for their investments and wealth. Individuals will find other ways to pass income and transfer wealth or push off selling businesses/stock/houses/etc. The tax on the wealthy may face significant hiccups in tax collection, even with a doubled budget for the IRS. This could be why the Biden Administration is putting such a priority on global corporate and minimum taxes. With all the tax minimization options available to wealthy individuals, it is questionable how we will pay for these social programs.

Likely scenarios resulting from Biden’s AFP Tax Plan

The tax starts to trickle down. We are possibly seeing it now with the lowered upper income bracket. Increased corporate taxes do not mean less money to the wealthy. It usually means higher prices, increased costs passed on to consumers, and more entry level jobs being handled by robots or self-service kiosks (think Wal-Mart self-check and McDonald’s ordering kiosks).If you have clients in the upper income brackets who share these concerns, the attorneys at Cantley Dietrich would enjoy having a conversation with you about how you can protect them from some of the challenges they will likely face in the next few years.

Citations

- Prof. Beckett Cantley (University of California, Berkley, B.A. 1989; Southwestern University School of Law, J.D. cum laude 1995; and University of Florida, College of Law, LL.M. in Taxation, 1997), teaches International Taxation at Northeastern University and is a shareholder in Cantley Dietrich, P.C. Prof. Cantley would like to thank Melissa Cantley and his law clerk, Reed Green, for their contributions to this article.

- Geoffrey Dietrich, Esq. (United States Military Academy at West Point, B.S. 2000; Brigham Young University Law School, J.D. 2008) is a shareholder in Cantley Dietrich, P.C.

- https://www.whitehouse.gov/american-families-plan/